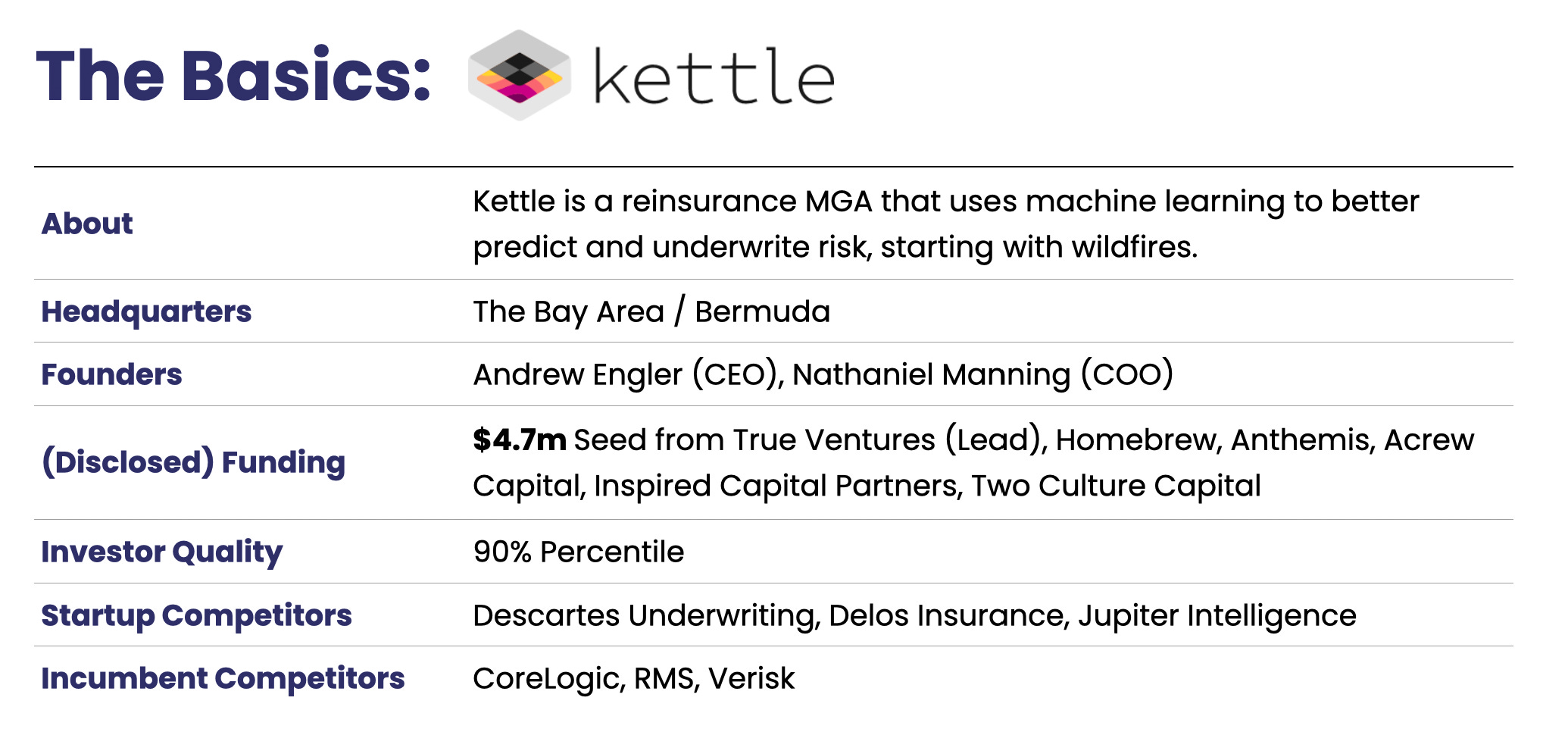

Kettle: the startup crazy (and smart) enough to underwrite the $10b+ wildfire re/insurance market

Re/insurers are backing away from wildfire risk. Kettle, on the other hand, is rushing in.

Welcome to The Future State: Insurance where we profile the startups rewriting the future of insurance. If you’re not subscribed, join below:

It’s not everyday that the assumptions underpinning a market are proven wrong to the point where incumbents are packing up and going home. But this is just what’s happening in wildfire re/insurance markets.

Traditional underwriting models weren’t built to handle once-in-a-lifetime fires every other year. This untenable risk is scaring insurers so much that states like California have stepped in, preventing primary home insurers from refusing policies to high-risk properties.

However, reinsurers (with their Bermuda licenses) have slid around regulations and swiftly exited markets – creating a supply vacuum when demand is at its all-time high. While traditional reinsurers are backing out of markets, the startup Kettle is racing in. Leveraging satellite imagery and swarm neural networks, Kettle has the chutzpah to underwrite the risk no one wants to touch. In this post, we dive into why investors like True Ventures, Homebrew, and Anthemis believe Kettle can capture the wildfire reinsurance market and outperform the incumbents who’ve been reinsuring catastrophes for centuries.

With superior underwriting and a supply vacuum (described below), we think it is more than reasonable that Kettle can take ~3-9% share of the U.S. wildfire reinsurance market. At traditional reinsurance valuations, this positions Kettle to become a billion-dollar business. Kettle suggests it may be able to operate at loss ratios far better than those of traditional underwriters and if this proves true, the case for a Kettle being a unicorn becomes that much easier.

If this sounds crazy, let us know.

Traditional reinsurers have outsourced much of their modeling to other firms, but why aren’t the modelers doing the underwriting? If you’re so confident, why aren’t you underwriting it? (Nathaniel Manning, COO, Kettle)

The Problem

Wildfires are increasing in frequency and intensity. Insurers and reinsurers don’t have up-to-date models to properly underwrite this risk leading them to increase premiums or pull out of markets.

Re/insurance markets are getting hit hard by wildfires. The losses due to wildfires in 2017, 2018, and 2020 were eye-popping. Munich Re estimates the total insured losses in 2017 and 2018 to be ~$15.5b and $18b respectively. RMS estimates the total insured losses in 2020 to be between $7b and $13b – predominantly due to the wildfires in California and Oregon. Compare this to the time period from 2010 to 2016, where the average insured losses were less than $1b.

The growing frequency and intensity of wildfires are forcing underwriters to completely rethink their assumptions. With the mounting losses, insurers are increasing premiums or backing out of markets altogether.

Underwriting priors were all wrong. Climate change is throwing underwriting models out of whack. With everything wiped out in 2017 and 2018, reinsurers are saying “I don’t understand this risk” or “Our models were wrong” and subsequently quadrupling prices for an adequate buffer. But those increased prices shouldn’t extend to downtown San Francisco properties. Their geographical targeting is out of touch. (Nathaniel Manning, COO, Kettle)

The fact of the matter is that wildfire underwriters haven’t been pushed to rethink their priors until recently – they’ve seen relatively small losses up until 2016. Climate change is shifting the assumptions their models are based on. Traditional models are based on historical loss patterns (which, by the above chart, would suggest little room for volatile shifts, especially in the order of 10x magnitude). Moreover, traditional models have also overweighted key data points like distance-to-brush. However, if you’re living in a high-risk zone, being 100 feet or 300 feet away from brush is not a material difference when the wind can propel wildfire embers up to a mile to start new fires. Incorrect assumptions like this have led to a growing protection gap in the wildfire insurance market, leaving people under-covered.

Swiss Re pioneered the idea of the ‘protection gap’ – the difference between the cover people have and the cover people should have. The total economic loss due to wildfires is vastly larger than that is properly insured. Just look at California and Australia: millions of acres burned, thousands of buildings destroyed, hundreds of people losing their lives. (Matthew Jones, Managing Director, Anthemis)

In 2017 and 2018, that gap was ~$5b and $6b respectively. While there exists a gap between insured and overall losses each year, the large gaps in 2017 and 2018 suggest that numerous exposed properties were under-covered or never covered in the first place. In theory, this suggests that certain areas require larger coverage terms (implying a larger market) or that underwriters need to be more clever in their underwriting methods.

Reinsurance is supposed to be the added layer of protection for insurance companies to protect against these catastrophes.

A brief reinsurance explainer: There's a common question whenever one digs into insurance: If an insurance carrier has a bad year (let's say a huge wildfire hits) and they have to pay out all the claims they promised to cover, how does that carrier crazy losses? That's where reinsurance comes in. Reinsurers insures the insurers. Reinsurance is a method to spread risk across insurance carriers so that no insurance carrier is exposed to the risk of one catastrophic event shuttering their business. Reinsurance is ultimately about understanding one topic really well and underwriting that one thing.

Climate change is demanding re/insurers to rethink their strategies and price unwanted risk in a more creative fashion. However, instead of rethinking their modeling, they’re increasing premiums or moving out of high-risk markets.

Through regulation, California has manufactured, unwittingly, huge demand for wildfire reinsurance. In 2019, California Senate Bill 824 prohibited primary insurance companies (that is, the Geicos and Allstates of the world) from canceling or refusing to renew home insurance policies for homes located in at-risk areas for up to one year after the state of emergency was declared – however, the state law could not prevent reinsurers from exiting the market.

The government put in place [Bill 824] saying primary insurance can’t drop policies in certain high risk areas where fires have already happened. Yet, reinsurers were able to back out of the market – as reinsurers are licensed in Bermuda! This created a demand suck as insurers couldn’t drop policies. With all the reinsurance contracts getting cancelled, all that risk is going back onto the primary insurer’s balance sheet. It’s a perfect why-now moment where the demand is off the charts. (Manning, COO, Kettle)

Reinsurers are running away from wildfire risk while Kettle is running toward it. The demand is high for wildfire reinsurance and market prices are high to compensate for previous losses. The only issue with this seemingly perfect moment is that, at the end of the day, wildfire risk is unwanted risk for a reason. Bad years (which are becoming more and more prevalent) could wipe away a company with too much risk on its balance sheet.

The Solution

Kettle is going after the ~$10b+ wildfire reinsurance market by better underwriting wildfire policies in a targeted fashion.

Traditional reinsurers have outsourced much of their modeling to other firms, but why aren’t the modelers doing the underwriting? If you’re so confident, why aren’t you underwriting it? (Manning, COO, Kettle)

Kettle is a Bermuda-licensed managing general agency (MGA) that uses a proprietary swarm neural network to more accurately underwrite wildfire reinsurance policies. Their swarm neural network – based on geospatial data and other data sources – is able to predict the occurrence, spread, and severity of wildfires. The model has been able to identify the top 20% of most dangerous wildfires with 100% accuracy.

A brief MGA explainer: A MGA can underwrite re/insurance policies on behalf of a carrier, taking a commission (typically 5-20%) on policies sold while bearing some of the risk. If we have a bad year of wildfires, Kettle won’t bear the brunt of the losses, though they will run the risk of not being able to find a carrier to back their policies.

Kettle takes a novel approach to constructing reinsurance policies. While traditional reinsurers will reinsure an entire carrier's book or a group of homes in the same zip code, Kettle provides targeted reinsurance (called Cat strips). Here, Kettle surgically removes high-risk homes that are geographically distributed across a state, making sure they’re not all in the same wildfire path. This circumvents the risk of ensuring too many properties that could be razed by a single wildfire. Theoretically, it's a win-win – Kettle insures what they believe to be mispriced properties and the carrier gets the (perceived) risk off its book.

With its pricing models, Kettle is able to better construct its book with a mix of low-risk and perceived-high risk properties at combined ratios 2-3x better than incumbents.

Additionally, as a reinsurance company, Kettle can reinsure globally, circumventing state-by-state regulations that bog down primary insurers.

You can write reinsurance anywhere in the world with a Bermuda license. As a primary, you have to deal with every single department of insurance and those can take years, incurring loads of legal fees in the process. (Manning, COO, Kettle)

A Bermuda license doesn't just mean Kettle can reinsure anywhere in the U.S., it can reinsure anywhere in the world. While a logical place to expand would be to go into new reinsurance products such as wind and flood, Kettle can (easily) branch into new geographical markets such as Australia, which is hard-hit with wildfires. As compared to primary insurance providers, Kettle will have a higher velocity for growth. The question lies in whether the products latch on.

The Risks

Insurance markets leave the riskier assets for new entrants. On one hand, Kettle believes it can underwrite these policies. While Kettle doesn’t bear all the risk, it needs regulations, relationships, and the climate to swing its way to enable its success.

So what could go wrong? Insurance after all is a risky business.

Putting your money where your mouth is.

Climate prediction analytics (such as RMS, CoreLogic, Jupiter Intelligence) are tackling the same problem in trying to better model and predict wildfires. Yet, they bear virtually no risk if the industry experiences a down year. While Kettle doesn’t bear all of the risk operating as an MGA, to achieve better margins it will likely need to start bearing more risk on its balance sheet. Financial engineering aside, bad years early on can shutter re/insurance businesses that lack a warchest. Though, at the end of the day, this is the exact bet Kettle is pitching itself on.

New product, old industry.

Reinsurance policies typically reinsure an entire book. Kettle is bringing a new type of reinsurance product to the market built on a new modeling system. Mix this with Kettle selling to an old school group of customers who inherently don’t like change, Kettle will need to get its foot in the door.

Distribution is theoretically easier in the reinsurance market than in primary markets. Effectively all reinsurance sales go through a small set of brokers versus the need to market heavily in direct-to-consumer markets. The hard part here is building the right relationships to champion Kettle’s products to get them into the market.

(Note: Easier distribution doesn’t necessarily mean higher margins, simply that what would be a variable marketing cost in a D2C format is not priced into the reinsurance policy.)

Looking to the Future

While the margins are historically low, Kettle projects better margins potentially accelerating its path to becoming a billion-dollar business.

We believe the opportunity in the U.S. market can help Kettle become a billion-dollar business one day.

Given that traditional insurance companies trade at 1x revenue, the math is quite simple here, Kettle would have to amass $1b in premiums to be valued at $1b (assuming at one moment, Kettle shifts from an MGA to a carrier).

But what share of the market is this? The total U.S. market size for wildfire insurance is elusive so we take the total losses paid out as a proxy. Over the 3 most recent years, the amount paid out has ranged from $7b to $18b. Losses make up a fraction of total premiums – expected combined ratios for reinsurers sit at 95-98% and expense ratios at 36%, suggesting loss ratios at about 60%. So, $1b in premiums would cover $600m in losses – approximately 3.3% to 8.6% of the total covered market.

The revenue multiple would likely increase due to Kettle's low volatility strategy, enabling them to operate at better margins. Hyper-focused reinsurers (such as Palomar) trade at 4x revenues. Moreover, insurtech companies that have gone public recently trade at higher revenue multiples. Lemonade trades at 54x forward-looking revenue and Root trades at (a probably more realistic) 4x forward-looking revenue. More generous valuations as compared to traditional incumbents would suggest Kettle would require even less of a market share to reach that $1b valuation.

Kettle has the opportunity to operate at higher margins. If they’re able to help recommend interventions to reduce the size and severity of wildfire events, they can capture value while creating a better consumer experience. In theory, you could use the team’s data models to place fire response teams at the top ten riskiest locations. You can tell PG&E that fires occur when the power remains on and when the wind goes above a certain threshold, PG&E could turn off the power as a precaution. (Adam D’Augelli, Partner, True Ventures)

At the end of the day, re/insurance isn’t just about pricing the risk. Preventing the calamity it seeks to model and intervening at the right time is a win-win for everyone. The promise of understanding wildfires is that one day we can prevent them. We will never be able to completely eliminate wildfires but we can implement the right practices to help mitigate the risks – and Kettle, down the road, can play a role in this.

While states impose mandates on securing homes against wildfires, Kettle has the opportunity to help provide another layer of protection to insurance companies and (transitively) to consumers – and become a billion-dollar company in the process.

Thank you to the team at Kettle (Nathaniel Manning, Andrew Engler, Son Le), as well as, Matthew Jones (Anthemis), Adam D’Augelli (True Ventures), and Jason Brooks (Co-Created).

Upcoming Posts (released every other week, in order):

Openly on how entering the market starting with high-value home insurance enables them to better build scalable underwriting infrastructure. Openly has raised $62.7m from Advance Venture Partners, Obvious Ventures, Gradient Ventures, and more.

Jetty on better distributing financial services to renters, helping them secure leases when they couldn’t otherwise, during a critical moment in history. Jetty has raised $40.5m from Ribbit Capital, Khosla Ventures, Valar Ventures, BoxGroup, and more.

Hover on how 3D modeling prompted new use cases for insurance carriers. Hover has raised $127.3m from VCs such as GV and Menlo Ventures, as well as, CVCs such as Nationwide, State Farm Ventures, and Travelers Insurance.

Subscribe to keep up to date!

Have questions, comments, or feedback? My email is harry@radicleinsights.com. Please reach out 🙏. Would love to hear your thoughts!

This is great. Our company creates a new wildfire Protection System. We designed an innovative water dispensing spigot that is not affected nearly as much as off the self sprinkler heads that are highly affected by wind, our Firestad spigots took 3 years to design specifically to work well in high winds. I would love to speak to Kettle in effort to see how we could help one another and mitigate the risk in high risk fire zones, saving homes, lives and losses to embers. I can be emailed at rcalonica@linkfireprotectionsystems.com